ACKNOWLEDGEMENTS

Portions of this report were commissioned by and prepared for the Center for Global Policy Solutions.

Drs. Peter Arno and Jeannette Wicks-Lim from the Political Economy Research Institute (PERI) at the University of Massachusetts-Amherst designed the research for this study. Dr. Wicks-Lim developed the methodological approach for the Social Security estimates with assistance from Dr. Arno, and conducted the data analyses. Drs. Arno and Wicks-Lim wrote this report in collaboration with CGPS staff.

Ms. Leah Smith, independent consultant, was retained to conduct interviews with and write profiles about former child Social Security recipients.

CGPS thanks Dr. Arno, Dr. Wicks-Lim, and Ms. Smith for their tremendous contributions to the final report.

The Center for Global Policy Solutions would also like to thank its staff members—Ms. Sarah Murphy Gray, Dr. Maya Rockeymoore, Dr. Algernon Austin, Ms. Simona Combi, and Ms. Roma Patel—for their help in developing this report.

This report was made possible as a result of the generous support provided by the Annie E. Casey Foundation.

Recommended citation: Center for Global Policy Solutions. (2016). Overlooked But Not Forgotten: Social Security Lifts Millions More Kids Out of Poverty. Washington, DC: Center for Global Policy Solutions.

EXECUTIVE SUMMARY

Social Security’s role in lifting millions of Americans out of poverty has been widely documented.[1], [2] However, the national focus on the program’s income assistance for senior citizens has obscured the fact that Social Security is also one of the federal government’s largest antipoverty programs for children. It serves more children than such discretionary programs as Supplemental Security Income (SSI),[3] and Temporary Assistance for Needy Families (TANF).[4]

In 2014, there were 3.2 million children under age 18 directly receiving Social Security income benefits either as the surviving dependent of a parent or guardian who had died, the dependent of a disabled worker, or the dependent of a retiree. Many of these children come from the nation’s most economically vulnerable households. As a result, Social Security is often the only financial safeguard protecting them from the harmful effects of poverty.

Yet, the number of children benefitting from Social Security is commonly underestimated. Using data from the U.S. Census Bureau’s Current Population Survey and the Social Security Administration’s Annual Statistical Supplement, this paper demonstrates an undercount in the number of Social Security beneficiaries under age 18. In fact, when children who are not direct beneficiaries but live in extended families that receive Social Security are added to the official figure, the number of children who benefit from the program doubles to 6.4 million. This represents 9 percent of all U.S. children under the age of 18 and 11 percent of all Social Security beneficiaries.

This study expands existing research about Social Security’s indirect role in lifting children out of poverty by examining its effect on those living in extended households.[5] It documents how the multi-generational impact of Social Security has been growing for more than a decade. By examining households where children were indirect beneficiaries along with those where they were direct beneficiaries from 2001 through 2014, this analysis demonstrates how Social Security has become an important and expanding income source, especially for children of color.

The following are the key findings:

Social Security is serving a growing number of children.

- In 2014, approximately 6.4 million children benefited from Social Security directly or indirectly, representing 9 percent of all U.S. children under the age of 18 and 11 percent of all Social Security beneficiaries.

- While there has been some growth in the number of direct Social Security beneficiaries under age 18, the majority of the increase is due to the growing number of children who are indirect Social Security beneficiaries.

- White children still represent the largest number of direct and indirect child beneficiaries of Social Security. However, the number of direct and indirect beneficiaries of Social Security who are children of color is on the rise.

- The number of indirect child beneficiaries in Latino households has grown, on average, by 4.2 percent annually between 2001 and 2014, indicating the increased importance of Social Security income for Latino families.

- Families that identify their ethnicity or race as other than White, Black or Latino have seen growth in indirect child beneficiaries of 12.7 percent annually.

- The number of African American and White children benefiting indirectly from Social Security is growing at a significantly slower pace than that of Latino children or children in households that identify as “Other.”[6] However, it is still growing more quickly than the number of African American and White children benefiting directly.

- Between 2001 and 2014, the number of African American children who directly benefit from Social Security has grown by 1.2 percent annually; the number of Latino children who directly benefit has grown by 2.4 percent annually; and the number of children of “Other” backgrounds who directly benefit has grown by 2.7 percent annually. The number of White children who directly benefit from Social Security has not grown over this period.

Social Security is lifting an increasing number of children out of poverty.

- Social Security substantially reduces poverty rates among all children in families that receive benefits by almost 20 percent (17.3%).

- For African American children, the poverty rate would increase to nearly 58 percent without Social Security benefits—an increase of more than 17 percentage points.

- For Latino children, the poverty rate would increase to nearly 45 percent without Social Security benefits—an increase of more than 17 percentage points.

- For White children, the poverty rate would increase to 39 percent without Social Security benefits—an increase in poverty of more than 18 percentage points.

- For children that identify their ethnicity or race as other than White, Black or Latino, the poverty rate would increase to nearly 29 percent—an increase of 13 percentage points.

Social Security contributes a significant percentage of the family income that supports children

- As household incomes have stagnated or declined over the past few decades, Social Security income has become a more important component of financial resources for children in families that receive direct and indirect benefits, contributing 39% to family income in 2014.

- This is true for all racial and ethnic groups and particularly for African American children where benefits contribute 46% to family income.

- For African American families with child beneficiaries, the share of total income provided by Social Security benefits has grown by 9.2 percentage points since 2001, the highest growth of all racial groups.

Children living in extended, multigenerational families are driving the growth in indirect beneficiaries.

- The large majority—about two-thirds—of indirect child beneficiaries live in multigenerational families consisting of three or more generations or in “skipped-generation” households that include families of grandparents and grandchildren only.

- The number of children living in multiple generational families has been rising over time, from 8 percent to 11 percent between 2001 to 2014. This growth in multigenerational families occurs across and within all racial and ethnic groups.

- In recent years, the fastest-growing racial/ethnic groups in the United States have been Asian Americans and Hispanics. Based on the significant growth in direct and indirect child beneficiaries, particularly among Latino and Asian American children, Social Security will become increasingly important to these children as the number of families increases for these populations.

In sum, as U.S. childhood poverty increased during the 2000s, Social Security played a crucial role in offsetting increased poverty rates across all racial and ethnic groups. When families needed it most, Social Security strengthened child economic security and helped to provide the critical necessities such as food, shelter, and clothing that children need to survive and thrive.

BACKGROUND

Social Security is typically considered a retirement plan for the elderly, and research has already documented how the program dramatically reduces poverty among adults age 65 or older. In 2014, for example, without their Social Security benefits, 14 million more of these seniors would have had incomes below the official poverty line.[7]

However, many Americans are unaware that millions of children receive Social Security as the dependent of a parent who has died, become disabled, or is retired. Even though Social Security is among the nation’s largest antipoverty programs that affects children, the program’s role in providing essential income for children is little known and rarely discussed.[8]

Social Security’s impact on child poverty and overall well-being are especially important to consider because of the current economic pressures affecting household living arrangements and our nation’s shifting demographics.

Studies show that the number of multigenerational households in the United States has increased by 70 percent since 1990.[9] This trend appears to be influenced by the aging of the population, household economic pressures resulting from a flattening in the growth of wages, increased immigration, and high rates of unemployment and underemployment.[10] The trend line for such living conditions continues to inch up fueled by economic pressures and the increasing number of racial and ethnic minorities, who are among the nation’s most economically vulnerable populations, and are thus more likely to live in multigenerational households.[11] Recent estimates indicate that by 2043, our nation will consist predominantly of families of color,[12] with the largest demographic shift occurring in the number of native-born Latino and incoming Asian American families.[13]

Research also indicates dramatic growth in the racial wealth gap over the past 35 years—meaning that the divide between assets owned by Whites and those owned by families of color has substantially grown. This increase in the racial wealth gap has occurred concurrently with the rise in three-generation households, whose children have become increasingly more reliant on programs like Social Security. As these trends have intensified, Social Security has become an indelible part of the larger safety net for American families, protecting against broader economic hardship and socioeconomic inequalities.

In general, for children under the age of 18 to directly qualify for Social Security benefits, they must be unmarried and meet one of the following requirements: they must have a parent who receives benefits on the basis of retirement or disability, or they must have a deceased parent who has an established work history of paying Social Security taxes.[14] In special cases, children may directly qualify for Social Security benefits based on their grandparent’s history of earnings.

Children over the age of 18 can continue to receive Social Security income if they have a disability that started before age 22. Additionally, they can continue to receive benefits until the age of 19 if they are still in primary or secondary school.

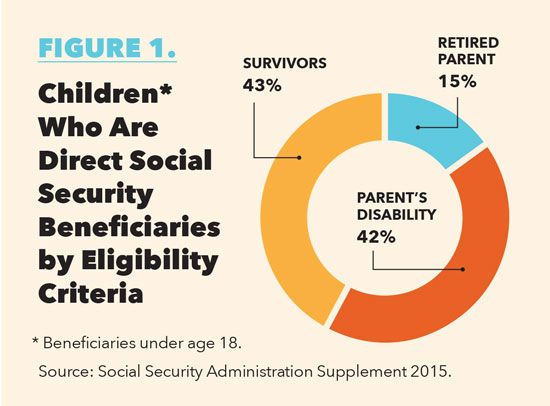

In 2014, there were 3,166,347 children under the age of 18 directly receiving Social Security benefits (see Table 1) with an overall average monthly benefit of $548.[15] However, the average amount of benefits varies by benefit type with children of retired workers receiving an average of $628 per month, children of deceased workers receiving an average of $821 per month, and children of disabled workers receiving an average of $335 per month. Child benefits are a major source of income for families receiving Social Security, on average accounting for more than half of a family’s Social Security income.[16] Of all child Social Security beneficiaries under age 18, the vast majority qualified as the dependent of a deceased or disabled worker, 43 percent and 42 percent, respectively.

Social Security keeps more than one million children out of poverty each year. Some studies have focused on the heavy reliance that children of color have on Social Security. The National Urban League found that Social Security lifts four times as many African American children as White children out of poverty.[17] According to the Center on Budget and Policy Priorities, families’ Social Security income kept 200,000 Latino children under age 18 above the poverty line in 2009.[18] Similar estimates exist for children in households that identify their ethnicity or race as “Other.”

It is important to note that children of color are disproportionately more likely than White children to receive Social Security as the surviving dependent of a parent who has died or as the dependent of a parent with a disability.[19] Additionally, children of color are more likely to receive retirement benefits as a result of being cared for by a grandparent, although the size of this recipient group is small.[20] The monthly Social Security check these children receive is vital for meeting their living expenses and keeping them out of poverty.

Clearly, Social Security is a tremendous economic benefit for children living in some of America’s most vulnerable households. But there is little doubt that Social Security’s importance in lifting children and their families out of poverty is undervalued in official statistics, by policymakers and by the American public.

Nationally representative surveys, including the Current Population Survey (CPS), the American Community Survey (ACS) and the Survey on Income and Program Participation (SIPP), generally underestimate the number of children under age 18 who benefit from Social Security, particularly for those who may not be direct beneficiaries but live in households that receive Social Security benefits.[21],[22], [23]

To date, there are only three other studies that examine the magnitude by which the positive income effects of Social Security extend to children both directly and indirectly. [24], [25], [26] Consistent with this past research, this study demonstrates that Social Security’s impact on children is much larger than is indicated by the number of direct child beneficiaries. In fact, when children who live in extended families that receive Social Security are included, the number of children who benefit from the program more than doubles to an estimated 6.4 million children.

This paper estimates the parameters of Social Security’s total impact on child poverty through an exploration of households in which children receive a benefit from Social Security indirectly as a result of their household relationship with extended family members such as an aunt, uncle, or grandparent who receives benefits. The analysis contends that even in households such as these, Social Security strengthens children’s economic security and helps to provide the critical necessities such as food, shelter, and clothing they need to survive and thrive.

This study also bolsters the thin body of existing research on Social Security’s indirect impact in two important ways. First, it documents how the multigenerational impact of Social Security has been growing for the last 14 years. Current underlying demographic and economic trends can be expected to support continued growth of the program’s impact over the next several decades. No other study has identified this expanding reach of Social Security.

Second, this report shows how Social Security has provided an important and increasing income source across different racial and ethnic groups over the past 14 years. There is a large gap in our knowledge of how different social groups benefit from Social Security because data from the Social Security Administration (SSA) on the race and ethnicity of recipients has increasingly become unreliable.[27] After 2009, the SSA stopped publishing program participation by race and ethnicity. As a result, researchers must rely on household survey data to provide a more complete demographic picture of program beneficiaries.

By exploring the impact of Social Security on child welfare broadly and its effect on children of color specifically, this research is expected to further educate the public and decision makers about Social Security’s critical role in addressing child poverty.

Social Security provides a safety net for more children than officially estimated

In 2014, roughly 6.4 million children benefited from Social Security in one of two ways: directly as beneficiaries or indirectly as dependents of households where at least one member received Social Security benefits. This represents 9 percent of all U.S. children under the age of 18 and 11 percent of all Social Security beneficiaries. These figures are more than twice the number reported by the Social Security Administration, which only reports direct beneficiaries. To put this estimate in perspective, Social Security is among the largest federal income supplements for children in the United States, serving more children than Supplemental Security Income (SSI),[28] and Temporary Assistance for Needy Families (TANF).[29]

As a program that contributes to the well-being of so many American children, it is important to understand the extent to which children’s lives are affected by the income provided through Social Security.

Social Security contributes significantly to families with children, but especially to families of color with children

As household incomes have stagnated or declined over the past few decades, Social Security income has become an even more important component of financial resources for families with children who receive benefits. Figure 1 illustrates the actual poverty rate among children in families receiving Social Security benefits in 2014 as compared to a measure of the poverty rate if those benefits were withdrawn.

As we can see, Social Security shields a large share of children from poverty. Without Social Security benefits for these families, people would fall further behind. The official poverty rate for child beneficiaries across all racial and ethnic groups would increase by about 17 percentage points without Social Security benefits, bringing the total poverty rate to an alarming 43 percent. For African American child beneficiaries, the poverty rate would increase to nearly 58 percent without Social Security benefits. For Latino child beneficiaries, the poverty rate would increase to nearly 45 percent without Social Security benefits—a rise of more than 17 percentage points.

For groups with lower poverty rates, like White and “Other” child beneficiaries, poverty rates would nearly double if income from Social Security were denied.

In 2014, Social Security contributed nearly two-fifths (39 percent) of the annual income for White families. For families of color, the contribution was even higher: Almost half the income (45.6 percent) of African American families with children came from their Social Security benefits. Social Security benefits as a share of total income for African American households with child beneficiaries has grown by 9.2 percentage points since 2001, the highest growth among all racial groups.

The significant growth in the percentage of household income from Social Security for African American families between 2001 and 2014 is concurrent with a drop in real (inflation-adjusted) median income for all African American families—from $39,000 in 2001 to $34,000 in 2014, the largest decline in income for any racial groups.

Further, the poverty rate for Black children with Social Security benefits (40.3 percent) is slightly higher than the poverty rate for White children without Social Security benefits (39.0 percent) [See Figure 2]. Therefore, while Social Security kept a greater percentage of White families from poverty, the same income provides much greater support in the African American family—demonstrating the necessity of such a program for all families, especially families of color.

Social Security’s safety net is catching more children as more children benefit indirectly from the income support.

A growing number of American children are relying on this vital social program from year to year. In 2001, 5.2 million children received Social Security benefits either directly or indirectly. By 2014, this figure had increased by 1.2 million, bringing the total number of children benefiting from Social Security to 6.4 million. This corresponds to an increase from 7.1 percent to 8.7 percent of all U.S. children from 2001 to 2014, respectively.

Families across the United States have seen an average annual growth rate of 3.5 percent for children benefiting indirectly from Social Security [See Table 2]. This accounts for nearly all of the 1.7 percent average annual growth rate in the number of children who have benefited directly and indirectly from Social Security over the past 14 years.

As the figures in Table 2 demonstrate, the number of children who directly benefit from Social Security has remained relatively stable over the period at approximately 3 million children. However, by disaggregating the data on direct beneficiaries of Social Security, we gain a larger understanding about how these benefits impact various households.

White families have seen no significant shift in the annual growth rate of direct beneficiaries of Social Security, but households that identify as African American, Latino, or “Other” have all experienced modest growth in direct beneficiaries since the turn of the millennium [See Figure 7]. Between 2001 and 2014, the number of African American children who directly benefit from Social Security has grown by 1.2 percent annually, the number of Latino children who benefit has grown by 2.4 percent annually, and the number of children of other backgrounds who benefit has grown by 2.7 percent annually. This indicates that even though White children still represent the largest number of direct and indirect child beneficiaries of Social Security, the number of children of color who are direct beneficiaries of Social Security is on the rise.

Overall, it is quite clear across all racial and ethnic groups that the increase in Social Security’s reach over the past 14 years is largely due to the rising number of children living in extended family households that receive benefits.

The number of indirect beneficiaries in Latino households has grown by 4.2 percent annually between 2001 and 2014, indicating the importance of Social Security income for Latino families. This growth means that more than 250,000 additional Latino children received Social Security benefits indirectly in 2014 than in 2001, bringing the total increase in direct and indirect Latino child beneficiaries to almost 400,000 children during this period.

The numbers are even more dramatic for children of families that identify as a race other than White, Black or Latino—for example, for Asian American families. These households have seen an indirect growth in child beneficiaries of 12.7 percent annually, the highest among every racial group surveyed. The number of beneficiaries within this group jumped from just 116,000 in 2001 to 428,000 in 2014. This means that children who identify as “Other” within the survey had the highest annual growth rate of both direct and indirect beneficiaries (6.3 percent) of any racial group. Their total beneficiaries grew by over 350,000—more than the growth in African American child beneficiaries and comparable to the increase in number of White and Latino child beneficiaries.

By comparison, the African American and White annual growth rates for indirect child beneficiaries were almost identical, 2.8 and 2.9 percent, respectively. As a result, the number of African American and White children benefiting indirectly from Social Security is growing at a significantly slower pace than that of both Latino and “Other” children. Moreover, the number of children who benefit indirectly and identify as “Other” has grown at four times the annual rate of those who identify as either African American or White (e.g. 12.7 percent vs. 2.8 percent).

The substantial rise in indirect child beneficiaries from Latino and “Other” households is concurrent with the growth of these populations in the United States.[30] Therefore, as we consider the solvency of Social Security for the coming generations, we must take into account the millions of children for whom this program is essential.

Social Security significantly reduces poverty among children in families that receive Social Security benefits, and this is true for children across and within racial and ethnic groups.

Social Security significantly reduces poverty for children in the United States across and within racial and ethnic groups, regardless of whether they benefit directly [Figure 8] or indirectly [Figure 9]. The percentage point reduction in poverty rates that we can attribute to Social Security is in the double digits for both the direct and the indirect beneficiary groups [See Table 3].[31]

African American children rely heavily on both direct and indirect Social Security benefits. Without them, over half of all African American child beneficiaries would fall into poverty. Moreover, Social Security reduces poverty by 15 percentage points or more for both direct and indirect child beneficiaries.

This trend is similar for Latino children who benefit either directly or indirectly: More than two out of every five would fall into poverty without Social Security; it reduces poverty by 15 percentage points or more for both direct and indirect child beneficiaries.

Similarly, approximately 40 percent of White children who benefit either directly or indirectly would fall into poverty without Social Security; it reduces poverty by about 18 percentage points for each of these groups of child beneficiaries.

“Other” indirect child beneficiaries are also largely kept from poverty by Social Security benefits. While their poverty rate is the smallest of any racial/ethnic group who benefits indirectly, this rate would nearly double without Social Security benefits. In fact, Social Security caused a greater reduction in poverty for all children of color who benefited indirectly than for all those who benefited directly.

It is clear that Social Security’s protective benefits for children have grown over time. The consistent reduction in the poverty rate of these children actually means that Social Security is lifting a growing number of children out of poverty. As shown in Table 3, Social Security prevented about 900,000 children who benefit both directly and indirectly from falling into poverty in 2001. By 2014, this number had grown to 1.1 million children. This pattern repeats within racial/ethnic groups. As childhood poverty has increased during the 2000s, Social Security has continued to play a crucial role in reducing the rise in poverty across all racial and ethnic groups [See Table 3].

Multiple-generation households with children receiving indirect benefits are increasing in number.

Nearly the entire growth in the number of children benefitting from Social Security is due to the rise in the number of children who benefit indirectly. One clear source of this growth is in the rise of multiple-generation families.

The large majority—about two-thirds—of indirect child beneficiaries live in what the Census Bureau considers multigenerational families, consisting of three or more generations or “skipped-generation” households that include families of grandparents and grandchildren only.[32] In this report, we refer to both types of families as multiple-generation households. [See Table 4]

The number of families with multiple generations has been rising over time across all racial and ethnic groups. For example, according to the U.S. Census, between 1990 and 2010, the number of multigenerational family households has grown from 3 million to 5.1 million, an increase of 70 percent.[33] During the 2000s, the percentage of children in these households has also increased across all racial and ethnic groups [See Table 5].

Multiple-generation households are becoming more prevalent. Two factors likely drive this trend. First, there are a growing number of adults classified as seniors in the United States [See Table 6]. Second, the plateau or decline in real median family income may push an increasing number of families to form multiple-generation households to pool resources as their budgets tighten. As indicated in Figure 5, real median family income, across all families with children, has declined by 8.6 percent, from $66,578 in 2001 to $60,410 in 2014 (inflation-adjusted).

Furthermore, prior research indicates that Social Security benefits for the elderly vary greatly depending on the race and gender of the recipient. Since African American, American Indian, and Asian Social Security recipients received at least $1,000 less than their White counterparts in 2014,[34] it is reasonable to conclude that children of color in these households also received less than their White counterparts as indirect beneficiaries. Promoting equitable adjustments to Social Security policy, would therefore provide a channel to reduce the higher rates of poverty among children of color relative to White children.

ANALYTIC APPROACH

The main objective of this study is to estimate the impact of Social Security on reducing child poverty. This analysis includes not only those children who are direct Social Security beneficiaries but also those who may benefit economically by living in households with other Social Security recipients. A special emphasis is placed on understanding how children of color, a rapidly expanding population, fare in households receiving Social Security.

All the estimates in this report are based on analysis of survey data from the Current Population Survey (CPS) and the Annual Statistical Supplements of the Social Security Administration (SSA) for the years covering 2001through 2014. The CPS is a household survey administered by the U.S. Census Bureau on behalf of the Bureau of Labor Statistics. The CPS surveys approximately 60,000 households per year from the U.S. civilian non-institutional population. In particular, this analysis uses the CPS Annual Social and Economic Supplemental Survey (CPS-ASEC) and applies the CPS March Supplemental sampling weights in order to make the data nationally representative.

The Annual Statistical Supplements, published by the SSA, report Old-Age, Survivors, and Disability Insurance (OASDI) benefits award data, which is referred to as Social Security. This is generally considered to be the most reliable source for the number of OASDI beneficiaries.

The major analytic challenge was to reliably adjust for underestimation of the number of children living in families receiving Social Security benefits—both direct and indirect beneficiaries. Indirect beneficiaries are defined as those children who live in families that receive Social Security benefits but are not direct beneficiaries themselves. This challenge is compounded by CPS methodology which limits participation in the survey to individuals who must be 15 years of age or older. Therefore, in brief, this analysis measured the number of direct beneficiaries age 15 through 17 in the CPS, compared and adjusted these figures to published SSA data, and then used this approach to account for all direct and indirect child beneficiaries through the age of 17.

A full report of the methodology can be found in the technical appendix.

STRENGTHS AND LIMITATIONS

As in all studies that rely upon survey data, by definition, the results are estimates. In particular, there are inherent limitations to the CPS that affect reported results. These include the CPS practice of limiting participation in the survey to individuals 15 years of age or older, and the difficulty that adult respondents have in distinguishing between their own benefits and additional benefits to children. However, wherever possible, we have adjusted our CPS estimates to account for published figures generated by the Master Beneficiary Records maintained by the SSA, which are considered very reliable.

Overall, there can be little doubt about Social Security’s powerful impact on children and their families’ economic wellbeing and the alleviation of poverty. This study also identifies a very significant trend in the increasing number of children who benefit from the Social Security program, one that to date has gone unrecognized and is likely to continue.

POLICY IMPLICATIONS

Social Security plays a vital role in support of families with children, contributing a significant portion of family income and alleviating and reducing poverty. Yet Social Security is viewed mainly as a retirement benefit for the elderly. Even its role in insuring the vast majority of workers through disability and survivor benefits is undervalued.

Overall, there is a lack of awareness on the part of the public, the media, policymakers, and private philanthropic institutions about Social Security’s key role supporting workers and their families over the entire life cycle from birth through old age. Greater public awareness of this perspective could have a significant impact on public policy by enhancing support for and strengthening Social Security and its myriad programs among all stakeholders.

In order to support these families, the Center for Global Policy Solutions proposes the following policy recommendations:

Increase Social Security Benefits for Those Who Need Them Most

Contrary to myths perpetuated in public debates about the program’s future, it is possible to strengthen Social Security’s finances while improving the lives of beneficiaries who are economically insecure.[35] This can be done by increasing revenues for Social Security by lifting the cap on taxable wages, compressing benefits for the highest-income individuals, increasing the amount employers and employees pay into Social Security by a minuscule amount over a 20-year period, and bringing all state and local workers into the system. This mix of revenue increases, as recommended by the Commission to Modernize Social Security, would in turn boost benefits for low-income and elderly individuals living in families with children. The Commission also advocates creating credits for workers who become temporary caregivers.

Extend Social Security Benefits to Post-Secondary School Students

Prior to 1981 when benefits to young adults were cut, sustained Social Security benefits made an undergraduate education possible for many students, and were especially important to students of color.[36] According to one estimate, reinstating such a program would cost less than 1 percent of taxable payroll for 75 years.[37] Thus, renewing Social Security benefits to young adults age 18 through 22 could encourage students to pursue higher education at a low cost to taxpayers.

Provide a Structural Unemployment Credit

Persistent unemployment and underemployment, especially for low-income families, creates gaps in income security and economic stability. To mitigate these gaps in Social Security benefits, a structural unemployment credit should be instated allowing workers to claim a credit for up to half of their average annual wage for up to five total service years. This credit would help alleviate the financial stress of part-time work on families, especially those with children who receive indirect Social Security benefits.

Conclusion

The collection, analysis, and evaluation of the research presented in this report clearly demonstrates Social Security’s crucial role in providing economic support and stability for millions of American children and their families. By contributing to household income, especially for families of color, Social Security has significantly alleviated poverty in the United States.

The paramount impact of Social Security is often invisible or obscured to the eyes of child and social welfare advocates as well as academics and policymakers.[38] Given Social Security’s importance in combatting child poverty in the United States, it is imperative that policymakers, practitioners, researchers, advocates, journalists, and the public better understand, prioritize, and strengthen the program’s vital role in providing economic stability for vulnerable children.

Works Cited

[1] Romig, K. (2015, November). Social Security lifts 21 million Americans out of poverty. Center on Budget and Policy Priorities. Retrieved January 15, 2016 from http://bit.ly/1WMPyX4

[2] Waid, M. (2015, July). Social Security Keeps Americans of All Ages out of Poverty: State-Level Estimates, 2011–2013. AARP Public Policy Institute, Fact Sheet 330. Retrieved March 1, 2016 from http://bit.ly/1JVMUdO

[3] Social Security Administration (2016, June). Table 3. Supplemental Security Income recipients, May 2016. Retrieved June 29, 2016 from http://bit.ly/29frDyu.

[4] Falk, G. (2016, March). The Temporary Assistance for Needy Families (TANF) Block Grant: Responses to Frequently Asked Questions. Congressional Research Service. Retrieved July 1, 2016 from http://bit.ly/29pnjQz.

[5] We use households and families interchangeably in this report. However, the analysis is based on only the primary family unit of children in the CPS, not the household unit.

[6] The race/ethnic category “Other” includes all other categories not listed in this report including Asian/Pacific Islander, Native Americans, and multiple race. White, Black, and Other are all exclusive of respondents who identify as Latino or Hispanic. Note that these categories changed over the 2002 and 2003 CPS surveys. Using only these aggregated categories helps to minimize inconsistencies over time.

[7] Romig, K. (2015, November). Social Security lifts 21 million Americans out of poverty. Center on Budget and Policy Priorities. Retrieved January 15, 2016 from http://bit.ly/1WMPyX4

[8] U.S. Department of Agriculture. (2016, June). Supplemental Nutrition Assistance Program Participation and costs. Retrieved June 29, 2015, from http://www.fns.usda.gov.

[9] Lofquist, D., Lugaila, T., O’Connell, M., & Feliz, S. (2012, April). Households and families: 2010 (BR-14). Washington, D.C.: U.S. Census Bureau, April 2012. Retrieved March 15, 2016, from http://bit.ly/29e6Ivi.

[10] For research on the rise multi-generational homes, see: Fry, R., & Passel, J. S. (2014, July 17). The Growth in Multi-generational Family Households (Rep.). Retrieved June 30, 2016, from the Pew Research Center: http://pewrsr.ch/29e6C74.

[11] Vespa J., Lewis J.M., & Kreider R.M. (2013, August). America’s Families and Living Arrangements: 2012 (U.S. Census Bureau, Report No. P20-570). Retrieved March 15, 2016, from http://bit.ly/29id0wE.

[12] U.S. Census Bureau. (2012, December 12). U.S. Census Bureau Projections Show a Slower Growing, Older, More Diverse Nation a Half Century from Now [Press release]. U.S. Census Bureau. Retrieved June 23, 2016, from http://bit.ly/29kn2N3.

[13] Brown, A. (2014, June 26). U.S. Hispanic and Asian populations growing, but for different reasons. Pew Research Center. Retrieved June 23, 2016, from http://pewrsr.ch/29hCdKL.

[14] Social Security Administration. (2016, March). Benefits for children (SSA Publication No. 05-10085). Retrieved April 20, 2016, from http://bit.ly/29knsTF.

[15] Social Security Administration, (2014, December). Number and average monthly benefit for children, by age and type of benefit (Table 5.A1.4). Retrieved from Annual Statistical Supplement to the Social Security Bulletin 2015. (2016, April). Retrieved from http://bit.ly/29iTJg5.

[16] Social Security Administration. (2015, March). Child beneficiaries and poverty. Retrieved from: http://bit.ly/29f3ZT8.

[17] Rawlston, V. (2000). The impact of Social Security on child poverty. Washington, DC: National Urban League Research and Public Policy Department.

[18] Sherman, A. (2010). Anti-Poverty Effects of Social Security by State, 2006-2008. Washington, DC: Center on Budget and policy Priorities.

[19] Rockeymoore, M., & Lui, M. (2011). Plan for a new future: The impact of Social Security reform on people of color. Washington, DC: Commission to Modernize Social Security.

[20] Ibid.

[21] Tamborini, C.R., & Cupito E. (2012, March). Social insurance and children: The relationship between Social Security, economic well-being, and family context among child recipients. Journal of Children and Poverty. 18(1):1-22.

[22] Martin, P.P. (2016, January). Why researchers now rely on surveys for race data on OASDI and SSI programs: A comparison of four major surveys. (Research and Statistics Note No. 2016-01). Social Security, Office of Retirement and Disability Policy. Retrieved May 1, 2016, from http://bit.ly/29rjyv8.

[23] Martin, P.P., & Murphy J.L. (2014, January). African Americans: Description of Social Security and Supplemental Security Income participation and benefit levels using the American Community Survey (Research and Statistics Note No. 2014-01). Social Security, Office of Retirement and Disability Policy. Retrieved May 1, 2016, from http://bit.ly/29iTRw2.

[24] Gabe T. (2015, January). Social Security’s effect on child poverty (CRS Report for Congress RL33289). Washington, DC: Congressional Research Service.

[25] Gabe T. (2008, January) Social Security’s Effect on Child Poverty. (CRS Report for Congress RL33289). Washington, DC: Congressional Research Service.

[26] Newcomb, C. (2003/2004). Demographic and economic characteristics of children in families receiving social security. Social Security Bulletin, 65(2), 28-48. Retrieved March 30, 2016, from http://bit.ly/29J44iQ.

[27] Martin, P.P. (2016, January). Why researchers now rely on surveys for race data on OASDI and SSI programs: A comparison of four major surveys. (Research and Statistics Note No. 2016-01). Social Security, Office of Retirement and Disability Policy. Retrieved May 1, 2016, from http://bit.ly/29rVB7h.

[28] Social Security Administration (2016, June). Table 3. Supplemental Security Income recipients, May 2016. Retrieved June 29, 2016 from http://bit.ly/29frDyu.

[29] Falk, G. (2016, March). The Temporary Assistance for Needy Families (TANF) Block Grant: Responses to Frequently Asked Questions. Congressional Research Service. Retrieved July 1, 2016 from http://bit.ly/29pnjQz.

[30] Brown, A. (2014, February). The U.S. Hispanic population has increased six-fold since 1970 (Fact-Tank: News in the Numbers). Pew Research Center. Retrieved from http://pewrsr.ch/29icIGj.

[31] Estimating characteristics separately for direct and indirect beneficiaries depends heavily on accurately dividing up the CPS into the two groups. As we discussed in the text, researchers are faced with several challenges in doing so (see Technical Appendix for further discussion). At the same time, because we have SSA published data, which relies on the program’s own administrative records, we can be confident in our estimates that roughly half of children who benefit from Social Security do so directly and half do so indirectly. Therefore, while our division of the child observations in the CPS into these two groups may be imprecise, the large size of each group (again, each roughly half) prevents us from making a grossly inaccurate characterization. Furthermore, the dramatic reduction in poverty appears for both of the groups we have identified. As a result, if we have misclassified a subset of children in each group, correcting for this would change the exact amount of poverty reduction that we observe, but not whether the level of poverty reduction is “large” or “small.”

[32] Vespa, J., Lewis, J,M., & Kreider, R,M. (2013, August). America’s Families and Living Arrangements: 2012 (U.S. Census Bureau, Report No. P20-570). Retrieved March 15, 2016, from http://bit.ly/29iU16J.

[33] Lofquist, D., Lugaila, T., O’Connell, M., & Feliz, S. (2012, April). Households and families: 2010 (BR-14). Washington, D.C.: U.S. Census Bureau, April 2012. Retrieved March 15, 2016, from http://bit.ly/29e6Ivi.

[34] Social Security Administration, (2016, March) Table3.c7a &3.c7b. Retrieved from Annual Statistical Supplement to the Social Security Bulletin 2015. Tables 3.C7a & 3.C7b. Retrieved March 10, 2016 from, http://bit.ly/29tX3pL

[35] Rockeymoore, M., & Lui, M. (2011). Plan for a new future: The impact of Social Security reform on people of color. Washington, DC: Commission to Modernize Social Security.

[36] Hertel-Fernandez, A. (2010). A new deal for young adults: Social Security benefits for post-secondary school students. Washington, DC: National Academy of Social Insurance.

[37] Ibid.

[38] American Academy of Pediatrics. (2016). Poverty and child health in the United States. Pediatrics. 137(4): e2 0160339. Retrieved May 10, 2016, from http://bit.ly/1X1m3WQ.

Profiles of Social Security Child Beneficiaries

Laura

Laura is a 54-year-old White woman who is devoted to building community in her central North Carolina town. A wife, mother, and social worker with an environmental advocacy organization, Laura grew up in a New Jersey suburb of New York City.

Her dad had a master’s degree and worked as a high-level engineer for a large telecommunications company. He was well paid and her family “never economized for any reason,” as far as she knows.

At 10 years old, Laura came home from school one day and learned that her dad died suddenly at his office. Laura and her sister, who was 8 at the time, began receiving a monthly check from Social Security.

Her mom was a “good steward” of the money and put all of it into college savings accounts for both of her daughters. Social Security wasn’t enough to live on, but Laura thinks it can offer the support that families with only one parent need to maintain stable lives and not abandon their dreams.

A few months after Laura’s father died, her family moved to southern California, where her father’s family lived. In their new neighborhood, which was “literally being built around them,” most families were single-parent households. Laura says that other moms in the neighborhood would complain about their ex-husbands and not getting enough child support, but her mom never complained about being a single mom.

The college savings accounts her mother set up with the Social Security checks enabled Laura to realize her dream of leaving California to go to college on the East Coast. She used the savings to pay for tuition, applied for scholarships, and took out a small loan that helped with living expenses.

Laura’s mom told her to go wherever she wanted, and that she’d pay for it as long as Laura graduated in four years. She is still grateful she was able to leave California, which she would not have been able to do without Social Security.

After college, Laura had a “really hard time.” The “emotional blow” of her father’s death, which she had never processed before, hit her suddenly in her twenties. This set her back for a long time—she says there was a decade of “push and go” and that it took another 10 or 15 years to recover from it.

Laura feels things would have been better if she had received counseling for emotional and psychological support when her father died. But she is grateful that she didn’t have a financial burden, which “could really have changed the trajectory” of her life.

When asked to describe Social Security in one word, Laura said “essential,” and then added, Social Security was “security to me.” She thinks that growing up feeling secure is critical to a productive life and that society overall is better off when everyone feels secure. Social Security gave Laura a sense of the broader community in the United States and taught her that we all take care of one another.

Elizabeth

Elizabeth is a 29-year-old White woman living in a West Virginia town. A social worker, she works with homeless people and has always been part of a “helper family” that likes to give back.

Elizabeth’s father died when she was an infant, her sister was 5, and her mother was 33. Her father’s death “was not in their long-term plans, and babies are expensive.”

Both Elizabeth and her sister received Social Security survivor benefits until graduating from high school, which really helped her family. Elizabeth’s mom worked part-time as a licensed practical nurse, which was her family’s only other source of income.

Elizabeth doesn’t want to think about how her family’s lives would have turned out without Social Security.

Without Social Security, her mom would have had to work longer and harder hours to support Elizabeth and her sister. Elizabeth says it “sucks in general” going from two parents to one, and that to almost lose another parent to working all the time would have been awful.

The monthly check from Social Security made Elizabeth feel better and gave her a sense of self-worth. She didn’t have to feel like she was selfish or a “horrible drain” on her family. This was especially important as Elizabeth often worried that she would do something to make her mom stop loving her and that she wouldn’t have a “back-up parent” to go to.

Senior year of high school changed everything. Between turning 18 in September and graduating high school in June, Elizabeth’s Social Security benefits started to go directly to her instead of through her mom. She saved most of this money, but did “splurge a little” to buy a dress for prom, the only dance that she went to in high school. Without Social Security, she would have felt guilty about asking to go “because of all the expenses that prom incurs.” Her all-time favorite photo is from prom night, which she considers a memory that she could never buy. In it, her grandpa, who never smiled in photos, is standing there with her “grinning like he just won an award.”

Elizabeth used some of the money she received from Social Security that year to pay college application fees and saved the rest to have a tiny cushion to use for gas and living expenses during her freshman year of college. She applied to as many scholarships as she could, any that she looked “even slightly qualified for,” which paid off. She received a Promise Scholarship that paid all of her tuition and a grant. She also got a part-time work-study job. Her mom was able to help a little with some college fees, and her sister bought her textbooks all four years.

After college, Elizabeth moved back to live close to her sister and mother. Her mom still works, and receives a “tiny little pension” from her dad’s job with the Division of Highways. But with her mom’s medical bills and expensive medications, Elizabeth and her sister must help pay their mom’s rent.

When asked to describe the importance of Social Security in one word, Elizabeth said “necessary,” a response borne of her experience both as a beneficiary and as someone who works with people receiving Social Security. She says there isn’t another option for people who can’t work and need assistance. She believes the United States needs this kind of safety net to keep people from abject poverty. She considers Social Security a “rickety ladder,” but an opportunity for people. Trying to limit Social Security will “keep people in poverty for longer or just make people literally die in poverty because they won’t have any means to be able to get out of that.”

Becca

Becca is a 22-year-old Black woman working on her master of social work degree.

Her parents immigrated to the United States from Haiti, raising Becca and her four siblings in Florida. When she was 12 years old, her mom passed away, causing “a hit on the family financially” because they didn’t have life insurance. Becca’s older brothers moved out to support themselves, but lived close by to help out. Her older sister stayed to help their dad raise Becca, the youngest by 11 years.

Then, a hurricane destroyed part of their family home just before the “economy started crashing down,” and Becca’s father was laid off. While he was unemployed, they received support from her brothers and others who knew her father and the work he did in the community as a pastor. After a few years, at age 63, he retired in order to receive Social Security benefits for himself and for Becca, who was by then 15 years old.

Soon after, Becca’s father married another Haitian who had recently become unemployed. Social Security was their only income during this time. It helped them pay for bills and food while Becca received free breakfast and lunch at school. When her friends would ask her about it, Becca had to explain that sometimes there wasn’t enough food to eat at home.

In eighth grade, Becca was recruited for a college preparation scholarship program, and by the time she was in high school she was taking honors classes and participating in many extracurricular activities. While her older siblings had to work when they were in high school, Becca didn’t have to because of the Social Security benefits. Her family wanted her to focus on school and do the best that she could to prepare for her future.

With a scholarship from high school, additional financial aid, and a work-study job, Becca was able to attend a small college in upstate New York. As a first-generation college student, Becca’s transition to college was “a little rough.” She was embarrassed about her financial background, and while she took pride in herself and where she came from, she was afraid of what her new peers would think. She felt like she led a “double life” between semesters at school and life at home.

Becca is concerned about the stigma attached to receiving Social Security and thinks it keeps people in need from seeking assistance.

Monthly Social Security benefits taught Becca the importance of budgeting, which served her well in college. While her friends went on shopping trips with borrowed money from their parents, Becca used her work-study money to buy needed winter clothes and boots. They didn’t believe that she came from poverty because she didn’t look like their perception of people in need.

Becca graduated with a degree in sociology and went straight into a master of social work program in pursuit of her dream to work with at-risk youth. She wants to create environments that support their strengths and build on their resiliency, all of which relates to her own experience growing up with Social Security.

When asked to describe Social Security in one word, Becca said “convoluted.” Navigating Social Security can be a “pain in the neck,” with age restrictions, eligibility rules, and changes from year to year. But Becca recognizes the importance of Social Security, which doesn’t exist in many countries. She especially appreciates its value to immigrants and their families, but acknowledges that it is not as easy for undocumented immigrants. She believes that “as long as people are contributing to their society or their community, they should be able to receive support without fear of being deported or mistreated.”

Ja’Ovvoni

Ja’Ovvoni is a 26-year-old black man living in a large Ohio city. He works as an e-commerce specialist at a printing company and describes himself as a “skateboard activist.”

Born in Ohio the third of nine kids, Ja’Ovvoni spent his first few years with his family in Florida where his dad still lives. When his parents split up, he moved back to Ohio with his mom, three brothers, and five sisters to live in his grandmother’s house—in “a mini community of kids”—and began elementary school.

While he was growing up, Ja’Ovvoni’s family received disability benefits for his younger sister who has spina bifida and Social Security retirement benefits for his grandmother. He spent a lot of time caring for his sister and his grandmother and became the “Cinderella of the family,” designated to help out while his mom and older siblings were working.

His grandmother had been a union worker in a steel factory and hearing her stories inspired him to want to work. He started working at age 16 and gave most of his money to his family. As long as he had a skateboard when he needed it, he was fine.

Ja’Ovvoni’s mom wrote a couple of bad checks in Ohio in order to buy things that they needed, like winter coats, and she wound up with a felony charge that made it very difficult to find stable work. By this point, his grandmother had gotten older and needed full-time care, as did his younger sister. And with eight other children to raise as well, Ja’Ovvoni’s mom decided to stay home to take care of everyone, so the family began to depend fully on Social Security, food stamps, child support, and other benefits.

Ja’Ovvoni thinks it is “crazy” that his sister’s disability was one of the only things keeping the family afloat. Without Social Security, his mom might have had no other options but to place him and his siblings into foster care.

Ja’Ovvoni’s family was pretty transient; their only stable living situation was when they lived in a house his grandmother owned until he finished middle school. When he started high school, around the time of the foreclosure crisis, his grandmother lost the house. If they didn’t have Social Security, Ja’Ovvoni thinks his grandmother would have probably lost the house much sooner than she did.

Twice, the family moved into a new place only to find out it was in foreclosure, and they had to move again. There were often maintenance issues, and their basement flooded in two different homes. They sometimes ended up in a homeless shelter for a month at a time. But his mom’s felony meant they could never get Section 8 housing, which Ja’Ovvoni says is “sad because if anybody needed Section 8, this lady did.”

Their first neighborhood was “like a 90’s TV show,” where everyone knew everyone, and if you got in trouble, everyone would know. The second was much worse, with gangs and violence more commonplace. Ja’Ovvoni turned to skateboarding to stay out of trouble, relieve stress, and stay active. He ended up working with the local community development center to create a project to fund a skate park in town. Since then, he and a friend have led skateboarding workshops and given away skateboards in what he describes as the “perfect stimulus package” to produce a skateboarding culture in the city.

Ja’Ovvoni went to community college for a few semesters but didn’t get his associate’s degree because he was interested in urban studies, which wasn’t offered there. He has been in his current position for four years. He lives with his older sister who has two kids and another on the way because she needs help paying her half of the rent with her upcoming maternity leave. He has never “ventured off” to get his own place because he is happy to stay with his mom and family and contribute, financially and physically.

When asked to describe Social Security in one word, Ja’Ovvoni said “beneficial.” He sees Social Security as a crucial asset for families and as part of the American dream.

Ja’Ovvoni calls Social Security a right, because “we are in this system where we all are contributing in some way to keep the bigger engine running.”

Benjamin

Benjamin is a 35-year-old White man, working as an elementary school music teacher, where he is committed to his work with students. He is full of energy, which he uses to give back as much as he can. He has a master’s degree in educational leadership and administration, is a consensus builder, and enjoys taking on leadership roles.

Benjamin grew up with his father, mother, and two younger brothers in the same working class Connecticut town his father did. His father made a good living as a lawyer working on high-profile cases about issues like urban education, so there was no need for his mother to work.

When Benjamin was 11 or 12, his mother passed out while shopping at a store, which was the first sign of her getting sick. Doctors didn’t know what was going on and thought that she had something similar to multiple sclerosis (MS). She became more and more off balance, and was soon declared disabled, unable to drive or work.

When Benjamin was 13 his father was treated for anxiety and put on a medication improperly without observation. Two weeks later he committed suicide.

Benjamin viewed this as a health crisis, but the life insurance company didn’t and denied his family’s claim. Even though his family had guarded against the loss of a parent, they only had Social Security to rely on in the end. To this day, more than 20 years later, Benjamin’s father doesn’t have a tombstone on his grave. His mother said it was a choice between buying a tombstone and putting food on the table, and that “one of those things was more necessary.”

Benjamin’s mother took whatever savings they had left and paid off the house so that they owned it outright and could stay there. Benjamin feels very fortunate that his family was well connected and that they had support through the process. Dealing with his father’s death itself was challenging, and having Social Security there to help carry them through was critical.

Benjamin’s mother remarried when he was 15. Benjamin says that it was “some miracle” that his mother met her second husband, who “gave up quite a bit of his life” to marry and care for her. He adopted Benjamin and his brothers when they were 16, 13, and 9. His adopted father had left the ministry and was unemployed, so Social Security continued to be their family’s only source of income.

As time went on, Social Security wasn’t enough to cover their expenses, and his family started using their house like a credit card, taking on “more and more” debt to pay for basic needs and his mother’s medical bills. Benjamin feels lucky that they didn’t end up homeless. His family talked about him quitting high school to work at a grocery store or in a ball bearing factory, which would have led to a very different life.

Eventually Benjamin’s mother was diagnosed with a rare genetic disorder similar to MS, and she is now paralyzed from the waist down. His adoptive father is a full-time teacher now after having worked odd jobs and substitute teaching.

Even with help from Social Security during those years, his mother and adoptive father are still living on the edge. If they hadn’t had Social Security, they would be “over the edge for sure.” They have been on the cusp of losing their house a few times and owe more on it than it will ever be worth.

The roof is “collapsing on top of them,” and recently the heat was shut off because they owed $2,000. Benjamin figured out a way to pay the bill on his teacher salary, and has continued to send money every month to help out a bit.

When asked to describe Social Security in one word, Benjamin said “necessary.” He knows that life can change in an instant. He had a very normal family with a working father and stay-at-home mother, and two years later his mother was disabled and his father was dead. His parents were better planners than most, but they ended up not having what they needed. He still gets worried that he will lose his job tomorrow and not know what to do. Social Security is not enough for his family, but it is a necessary aid. Benjamin thinks that as a society, we need to consider the idea that “when we all do better, we all do better.”

Technical Appendix

Estimating the number of child beneficiaries from the Current Population Survey

officialAll the estimates, unless otherwise noted, in this report are based on survey data from the Current Population Survey (CPS) and the Annual Statistical Supplements of the Social Security Administration (SSA) for the years covering 2001 through 2014. Information on these data is available online at www.bls.gov/cps and www.ssa.gov, respectively. The CPS is a household survey administered by the U.S. Census Bureau on behalf of the Bureau of Labor Statistics of the Department of Labor.

The CPS surveys approximately 60,000 households, and samples from the U.S. civilian non-institutional population. We specifically used the CPS Annual Social and Economic Supplemental Survey (CPS-ASEC), which is administered in March each year.

The CPS-ASEC collects data on all respondents’ income sources, including their Social Security income. Starting with the 2002 survey, which inquires about the previous calendar year, the CPS-ASEC asks not only about the amount of benefits but also the reasons for receipt. The CPS-ASEC also collects such information as age, race/ethnicity, and other family income, along with a wide range of other demographic, social, and economic characteristics at the individual, family, and household levels. In all the analyses in this report, we apply the CPS March Supplemental sampling weights in order to make the data nationally representative.

The Annual Statistical Supplements, published by the SSA, reports OASDI benefit award data (referred to in the main text of this report as Social Security) based on the Master Beneficiary Record (MBR), the major administrative database for the Social Security program. These data are generally considered to be the most reliable source for the number of OASDI beneficiaries.

Direct child beneficiaries

We use the CPS-ASEC to identify children who directly receive Social Security benefits. The CPS collects information about Social Security receipt only from children 15 years or older. Additionally, the CPS asks adults if they receive Social Security benefits on behalf of children (though not which specific child or children) in their families.

To test the quality of the CPS survey data, we begin by estimating the number of 15- through 17-year-old direct beneficiaries. This is because, as noted above, the CPS actually collects data on the direct receipt of benefits for children in this age group. We should therefore be able to produce estimates that are reasonably close to the figures published by the SSA on this age group.

For this analysis, we include all 15- through 17-year-old children who report receiving Social Security directly and all 15- through 17-year-olds whose parents report receiving Social Security on behalf of children in their family. We then compare this to SSA’s published figures in its Annual Statistical Supplements. The SSA figures are in column 2 of Table A.1. Our CPS estimates are in column 3.

The ratio of these two sets of figures, presented in column 4, shows that there is a significant degree of under-reporting in the CPS. Column 4 of Table A.1 shows that the CPS estimates are between 38 percent and 55 percent of the SSA figures. One reason for this level of under-reporting is the fact that parents with children under age 18 may receive their own benefits in combination with benefits for their children; they may not, therefore, distinguish between the two.[i], [ii]

Due to the difficulty of identifying child beneficiaries, we include among direct beneficiaries those children who live with their parents and who receive OASDI benefits. Inclusion of these children among direct beneficiaries is reasonable because there is a high likelihood that the children of parents who receive OASDI would also receive some benefits (see eligibility discussion above), with one exception: When in families where adults receive OASDI benefits as surviving or dependent children themselves, it is less likely that their children also receive benefits. This is because the eligibility for benefits received by the adult, due to his/her status as a surviving or dependent child would need to extend to the insured worker’s grandchild. The requirements for a grandchild to be eligible for benefits are more restrictive.[iii] For this reason, we exclude from our group of direct child beneficiaries those children whose parents receive benefits due to being a surviving or dependent child.

Our estimates of the number of children who live with their parents and whose parents receive Social Security for reasons other than being a surviving or dependent child are shown in column 5 of Table A.1. We then combine the two groups of direct child beneficiaries in column 6. The ratio between the number of 15- through17-year-old direct beneficiaries (column 6) compared to the SSA published figures (column 2) now ranges between 0.85 and 1.03 (see column 7). In sum, based on this more inclusive definition of 15- through 17-year-old direct beneficiaries, the CPS appears to estimate closely the number of children, 15 through 17 years old, who are direct Social Security beneficiaries.

After consulting with researchers at the Office of Retirement and Disability Policy of the Social Security Administration about the degree to which the CPS estimates vary from the SSA published figures, we feel confident that the CPS does a reasonable job of identifying direct child beneficiaries.[iv]

We next turn to the question of how well the CPS estimates the number of direct child beneficiaries under 18 years old—the group that is the focus of our study. Because the CPS does not ask directly about the Social Security benefits of children under 15, we can expect that the ability of the CPS to identify direct beneficiaries in this group to be lower.

To identify direct child beneficiaries, infant through 17 years old, we use the same approach as above. That is, we include in our sample all children that fall into any one of three groups:

- children who report receiving benefits directly,

- children whose parents report that they receive benefits on behalf of their children, and

- children who live with parents who receive Social Security for reasons other than being surviving or dependent children.

In Table A.2, we provide figures analogous to those in Table A.1, this time for infants through 17 year olds. We can see that the rate of under-reporting without including the third group listed above is high, with only one-quarter to one-third of the direct beneficiaries being identified by the CPS (see column 4 of Table A.2). When we add in infant through 17-year-old children who live with parents who receive Social Security for reasons other than being surviving or dependent children (see columns 5 and 6), our CPS estimates of direct beneficiaries approximate the SSA figures much more closely (see column 7).

At the same time, our more inclusive definition of direct beneficiaries causes our CPS estimates to overstate the number of direct child beneficiaries. To adjust for this, we weight the observations of children in the third group listed above (those whose parents receive Social Security) so that when combined with groups 1 and 2, our estimate of the number of direct beneficiaries equals the SSA published figures. The formula for this weight is: ((col 2 – col 3)/col 5). These weights are presented in Table A.3.

We use the weights in Table A.3 to adjust all the figures by race/ethnic grouping. In other words, we assume that the adjustment factor that we use for all children is appropriate for groups within race/ethnicity. We do this due to the absence of reliable SSA administrative data by race/ethnicity to which we can compare our figures.

The SSA stopped reporting figures by race/ethnicity separately after 2009; therefore we do not have any published data with which to compare our figures after 2009. Moreover, starting in 1989, the vast majority of applications for Social Security numbers were created when a child was born through the Enumeration at Birth (EAB) program. The EAB program, however, does not provide the SSA with race or ethnicity data. Some individuals may submit a new application for a Social Security card later in life at which point, individuals may report their race and/or ethnicity. However, reporting one’s race/ethnicity is voluntary and is, according to SSA researcher Patricia Martin, “insufficient for maintaining the overall reliability of administrative race/ethnicity information.”[v]

Indirect child beneficiaries

The number of children who are indirect beneficiaries is simply the number of all children who live in families that receive any Social Security income minus the number of direct child beneficiaries.

To estimate characteristics among indirect child beneficiaries, we include in our sample all children that fall into any one of three groups:

- children who do not report receiving benefits for themselves and who live with parents who receive benefits for themselves (and not on behalf of children);

- children who do not report receiving benefits for themselves and who live with relatives who receive Social Security for themselves (and not on behalf of children); and

- children who live with parents who receive Social Security as a surviving or dependent child.

Based on our discussion above, we know that most of the children in the first group should be included among the direct beneficiaries (as implied by the adjustment factor in Table A.3). Therefore, when we estimate characteristics of this group (e.g., the percent of multigenerational families among indirect beneficiaries) we need to weight the children in that group to represent a much smaller share of indirect beneficiaries than their actual count. In this case, the adjustment factor (weight) we apply to children in this first group is: 1 – (adjustment factor).

In order to feel confident that we are accurately identifying children who indirectly benefit from Social Security, we do one additional test to check the quality of the Social Security benefits reporting in the CPS. We compare the number of adult (18 years and older) Social Security recipients as reported by the SSA to the number identified in the CPS (see Table A.4). We focus on adults specifically because their receipt of Social Security benefits is the primary mechanism by which we identify families with children who may be indirect beneficiaries of Social Security. We can see that the CPS approximates the SSA figures reasonably well, if under-reporting modestly.

Based on these explorations of the data, we feel confident that with our adjustments we can identify fairly well, if somewhat under-estimating, the number of children who benefit directly or indirectly from Social Security.

Estimating characteristics separately for direct and indirect beneficiaries presents a greater challenge than estimating level numbers. This is because, in order to estimate the level numbers we can, at minimum, difference out the SSA’s published data (based on the program’s administrative records) on direct child beneficiaries from the overall number of all children identified in the CPS living in families in which at least one person receives Social Security benefits. This latter measure does not require respondents to differentiate between child or adult benefits—only whether or not the family receives any Social Security (OASDI) benefits.

Estimating characteristics separately for direct and indirect beneficiaries, on the other hand, depends strongly on accurately dividing up children identified in the CPS living in families in which at least one person receives Social Security benefits into the two groups. As we have discussed above, researchers are faced with several challenges in doing so. For example, the researcher must rely on reporting of Social Security receipt by adults on behalf of children to identify these children. Our comparisons of the CPS data to SSA published data indicate that parents do frequently indicate—inaccurately—that they do not do so. As a result, we present only a limited number of estimates of characteristics for each group of child beneficiaries separately (see main report, Figure 7).

We do, for example, provide a comparison in the main report of poverty rates among these two groups of child beneficiaries when we include and then exclude their Social Security income. As we note in the main text, we observe for each group a large reduction in poverty when their Social Security income is included relative to when their Social Security income is withdrawn from their family incomes (see main report, Figures 8 and 9). Furthermore, because we have SSA published data, which relies on the program’s own administrative records, we can be confident in our estimates that roughly half of children who benefit from Social Security do so directly and half benefit indirectly. The large relative size of each group suggests against characterizing either in a grossly inaccurate way, despite having imprecise estimates. As a result, if we have misclassified a subset of children in each group, correcting for this would change the exact amount of poverty reduction that we observe, but not whether the level of poverty reduction is “large” or “small.”

Interview Methodology

The research conducted for the production of the profile pieces was done through phone interviews with people who benefitted from Social Security as children. The interviewer and the Center for Global Policy Solutions did outreach across diverse networks in order to identify potential interviewees. Six people responded to the outreach with interest in being interviewed.

Each interview was conducted and recorded on the phone via conference line, and then transcribed for analysis. The calls lasted between 20 minutes and one hour, depending on the availability and interest of the respondent. An interview guide was developed, which the interviewer used, along with follow-up questions that allowed for more specific answers based on the information that interviewees shared.

At the beginning of each interview, respondents had the chance to agree to being recorded before the interviewer started the audio recording. The interviewer explained that the main purpose of the recording was to help with the profile pieces for this national report. Each respondent agreed and signed a waiver allowing for the use of the audio for the report and other purposes in the future. The interviewer also explained the option of using the respondent’s full name, first name, or pseudonym in the report, and each noted their choice on their consent form.